Homes for Heroes vs. ARC Realtor Rebate

When you’re buying or selling a home, every dollar counts. That’s where real estate rebate programs come in—they give you cash back on one of life’s biggest purchases. Two popular options are the Homes for Heroes program and the ARC Realtor Rebate. Let’s break down how each works, what you’ll save, and which might be the better choice for your situation.

Homes for Heroes Rebate: How it Works

The Homes for Heroes program connects specific professionals with real estate agents and lenders who offer discounts on their services. If you’re a teacher, firefighter, healthcare worker, military member, or first responder, you qualify for their network.

Here’s the catch—you don’t get to pick your own agent. Homes for Heroes assigns you someone from their network based on your location. Sure, you can ask your current agent to join their program, but there’s no guarantee they’ll be accepted. Once you’re matched with an agent, you’ll work with them throughout your home buying or selling process.

The savings come as rebates after closing. For home purchases, you’ll get a check for 0.7% of your home’s purchase price. On a $300,000 home, that’s $2,100 back in your pocket. If you’re selling, you’ll receive a 25% discount on your agent’s commission at closing.

How to Apply

Getting started is straightforward—fill out a form on their website with your contact info and profession. A representative will call you within a day or two to verify your eligibility and match you with local agents. Remember, you need proof of your qualifying profession, like a work ID or pay stub.

Discounts Offered

Beyond the real estate agent rebate, you can stack savings by using other Homes for Heroes providers:

- Lender fees: Average $500 rebate

- Home inspection: Around $50 back

- Title services: Varies by provider

- Total average savings: $2,400 per transaction

The more services you use within their network, the more you save. Just keep in mind you’re limited to their approved providers.

ARC Realtor Rebate: How it Works

The ARC Realtor Rebate takes a different approach—and it’s open to everyone, not just certain professions. The best part? You can work with almost any realtor you want since ARC has a massive network of participating agents.

Your rebate amount depends on your home’s price, following a clear tier system. The higher your home’s value, the bigger your rebate. And unlike some programs, ARC’s rebates never cap out—even on multi-million dollar properties. One major perk is speed. While other programs might make you wait weeks for your rebate check, ARC promises a 2-day turnaround after closing. They’ll also match or beat any other rebate offer you find, giving you serious negotiating power.

How to Apply

Registration takes just a few minutes through the online form. You’ll provide basic info about your home search or sale, then ARC connects you with participating agents in your area. If you already have an agent in mind, they can likely work with them too—ARC’s network is that extensive.

Discounts Offered

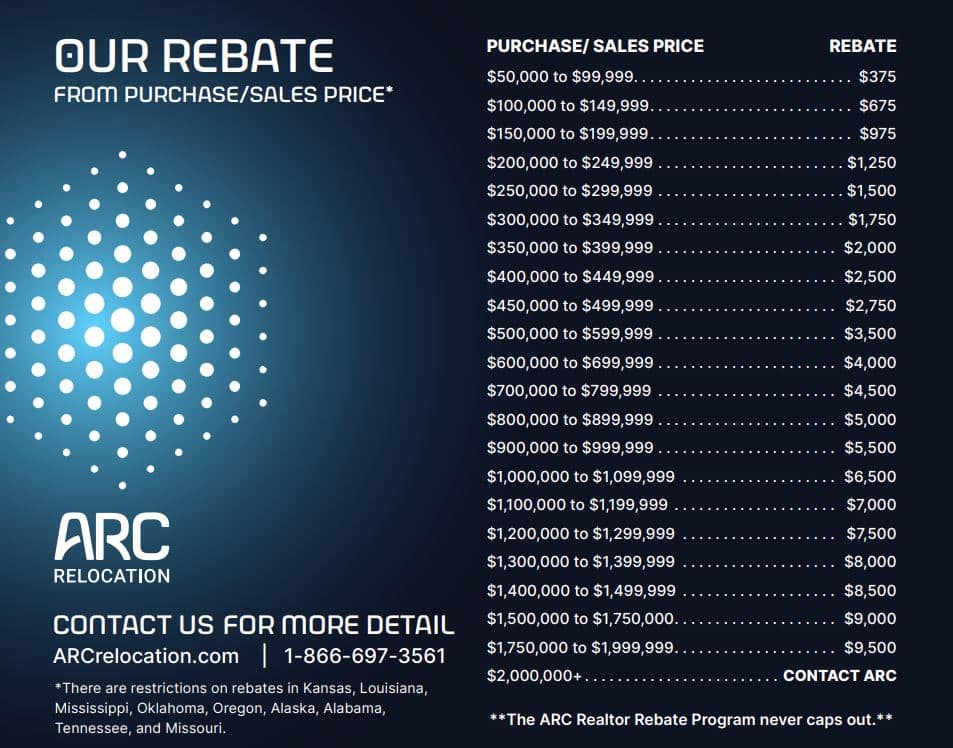

ARC’s rebate structure is transparent and easy to understand:

- $150,000-$199,999 home: $975 rebate

- $300,000-$349,999 home: $1,750 rebate

- $500,000-$599,999 home: $3,500 rebate

- $1 million+ home: $6,500 and up

These amounts apply whether you’re buying or selling, and there’s no limit on the maximum rebate for luxury properties.

Why Choose the ARC Realtor Rebate

Several factors make the ARC Realtor Rebate stand out from the Homes for Heroes program and other competitors.

First, there’s the freedom to choose your agent. You’re not locked into working with whoever gets assigned to you—you can pick someone you trust, someone recommended by friends, or keep working with an agent you already know. This flexibility alone makes a huge difference in your home buying experience.

The rebate amounts often work out better with ARC too, especially for mid-range and higher-priced homes. While Homes for Heroes offers 0.7% back, ARC’s tiered system can deliver more cash on many transactions. Plus, the price-matching guarantee means you’ll never leave money on the table.

Speed matters when you’re dealing with moving expenses and closing costs. Getting your rebate in just two days instead of waiting weeks helps with cash flow during an already expensive time. Other rebate programs through large companies often involve bureaucratic delays—ARC keeps it simple and fast.

You also don’t need to prove you work in a specific field. Whether you’re an accountant, artist, or engineer, you qualify for the same rebates as everyone else. This inclusivity means more people can access meaningful savings on real estate transactions. Another advantage is transparency. Some rebate programs hide their rates or make you jump through hoops to find out what you’ll actually save—ARC publishes the entire rebate schedule upfront, so you know exactly what to expect before you even register.

The price-matching policy deserves special mention too. Found a better rebate offer elsewhere? ARC will match or beat it, period. This takes the guesswork out of shopping around for the best deal and ensures you’re getting maximum value.

Working with ARC also means avoiding restrictions found in other programs. Some rebate services limit you to specific real estate brands or franchises, while the Homes for Heroes program restricts eligibility to certain professions. ARC’s open network and inclusive approach mean more options and fewer headaches for you.

Register Today

Ready to save thousands on your next home purchase or sale? The ARC Realtor Rebate program makes it easy to get cash back without sacrificing quality or choice in your real estate transaction. Our combination of flexibility, speed, and competitive rebates sets them apart from programs like Homes for Heroes that come with more restrictions and requirements.

Don’t leave money on the table—register for the ARC Realtor Rebate today and see how much you can save. With an extensive network, fast payouts, and price-matching guarantee, you’re practically guaranteed to come out ahead.